What strings to attach to governments’ equity support?

By Aleksandar Simić and Rens van Tilburg

The European Commission is working on a framework for equity support, the next generation of government support measures for companies. This blog discusses the US experience with equity support for car manufacturers in 2008, the current developments with the airline industry, as well as current different proposals of this nature from the leading think tanks.

Digital central bank money doesn’t need laundering

Money is

dirty. Literally. Empiricalfindings (also here

and here) show that various strains of

bacteria, viruses, and fungi live on our banknotes and coins. This

disease-transmission channel is especially relevant now with the

COVID-19 pandemic

that killed thousands

of people worldwide.

COVID-19 will test the new financial architecture of the euro zone. Since the euro crisis, new instruments have been developed, such as the European Stability Mechanism (ESM) and the ECB’s Outright Monetary Transactions (OMT). OMT being the bazooka the ECB created, but never needed to use, after Mario Draghi in 2012 pledged to do “Whatever it takes to save the euro”. The question now is whether policymakers are willing to use them.

Asset tracking, which includes monitoring

the identity, location and condition of individual components or products, can

effectively extend the economic lifetime of products, thereby bringing a host

of benefits to companies. This is according to new results launched today by

the Community of Practice (CoP) – consisting of Rabobank, Allen & Overy,

Schiphol Group, Avery Dennison on behalf of the NBA (The Royal Netherlands

Institute of Chartered Accountants), Circularise, Everledger, Fairphone,

Sustainable Finance Lab and Circle Economy.

Looking at the benefits of asset tracking

for Product-as-a-Service entrepreneurs, the CoP sets out to tackle the

complexity of asset tracking by uncovering the best technologies and mapping

the financial and legal implications of the process. To ensure that the

research outcomes reflected reality they teamed up with Fairphone, who aims to

launch a Fairphone-as-a-Service to businesses using their recently launched,

easy to repair modular Fairphone 3.

In the past decade, tech companies became ubiquitous not only in our daily lives but also in the global economy. By the beginning of the 2010’s the list of largest companies in the world as measured by market capitalisation was dominated by oil producing companies and financial services.[1] In 2019 however, seven out of the ten largest companies in the world are tech companies.[2] Along with rising economic power, their public image has shifted.

Digitization and the ‘sharing economy’ once went hand in hand, promising a new and better society. Inspired by San Francisco’s hippie culture, the entrepreneurs of Silicon Valley portrayed an image of do-gooders. But how did we get from the cozy sharing platforms of the early days of the internet to the imposing and omni-present corporate platforms of today? We show that they are a logical result of the forces at work in the platform economy.[3] And these same forces lead these tech companies into the financial sector in search for (personal) financial data.

Where does the money come from? Sources of finance for the European energy transition

We analyse

supply and demand in major scenarios for the European energy transition until

2050. We then contrast it to the available sources of finance. The good news is

that the private money is – in principle – available to finance the investments.

The bad news however is that does not (yet) come in the forms and shapes that

the European energy sector would need it. Changing the situation requires

action from both the private and the public sector in the coming years[1].

We know how much we need

Many

studies highlight the large amounts of investment into energy supply and demand

that is required. An innovation-led sustainability transition requires both

investments in invention and innovation as well as diffusion in a diversified

financial system (Polzin et al., 2017). Our review reveals that under the

individual investment and lending mandates the money is available. Many of the

scenario-based analyses explicitly or implicitly neglect the sources of finance

rather focusing on aggregate investment needs. For example McCollum et al. (2018, p. 591) state that ‘[…] given the nature of these models, we expressly address the

question of ‘Where are the investment needs?’, not ‘Who pays for them?’’.

The money is available,

but…

Our analysis

further shows, on the one hand, that the volumes are available in the order of

magnitude needed for a successful energy transition, especially when it comes

to institutional investors. On the other hand, the numbers also reveal a

qualitative mismatch. There is ample capacity to invest in scaling mature

technologies, but there are shortages in (upstream) innovation finance,

especially research, development and demonstration (RD&D) as well as

venture capital and private equity. There the amounts are smaller, but the

downstream impacts are not. There is no quantitative issue in freeing up these

resources and a little will go a long way in solving the most urgent

bottlenecks. However typically the types of finance suitable for funding experimentation

are not so easy to mobilize in Europe’s highly institutionalized, bank based

and regulated financial sector (Elert et al., 2019).

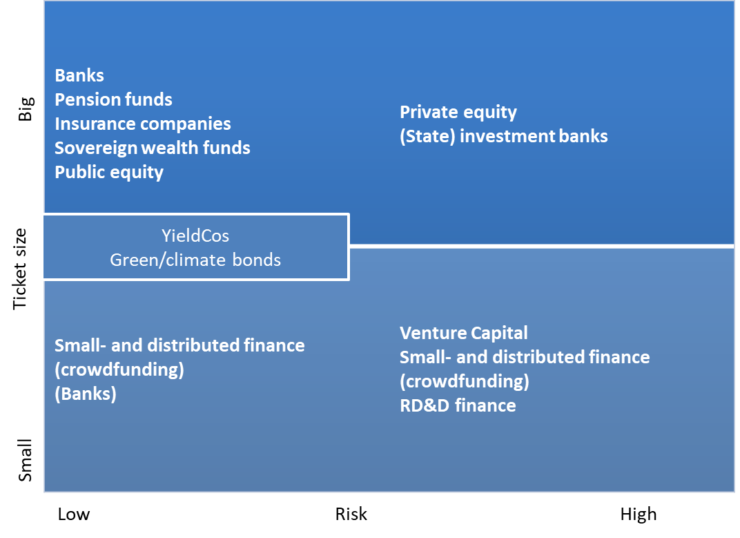

Who can do what?

It becomes apparent

from our review that there is plenty of financing available especially in the

later stages of technology lifecycle (see Figure 1) when the risks involved are

comparably low. That means even within the current composition of equities,

bond and alternative investments, institutional investors could engage in

financing large-scale (low-risk) renewable energy projects (Röttgers et al.,

2018). An effective reform of regulation

and governance to allow these investors to engage more in unlisted long-term

equity and debt will make ample funding available to scale the necessary

technologies. These could be realised through intermediate channels such as

green bonds or YieldCos but institutional investors also heavily engage in public

equity markets another underutilized source (La Monaca et al., 2018).

In the

earlier stages of the technology lifecycle (with considerable risks) the

problem is more urgent. Here only hardly scalable solutions such as small and

distributed finance and venture capital are available. These are also able to

address significant early stage risks (see Figure 1). Larger ticket sizes and higher

risks can only be handled by (state) investment banks and some private equity

funds. State investment banks have the potential to scale-up their investments

significantly. However, their main role would be in mobilising private finance

through co-investments, signalling and education (Geddes et al., 2018).

Figure 1: Sources of finance

for the energy transition (framework adapted from (Criscuolo and Menon, 2015))

Unlocking the potential

Our review yields

three major ways of unlocking the potential of different sources of finance.

First, initiatives promoting socially responsible investments from within the

sector (such as pension funds and sovereign wealth funds) that base their

investments also on ESG criteria could be scaled up (G20 Green Finance Study Group, 2016) An innovation-led energy transition

needs risk-carrying capital in smaller tickets (Owen et al., 2018;

Polzin et al., 2018). That needs freeing equity from

individual retail investors or institutional funding from pension funds,

insurance companies or sovereign wealth funds (Polzin et al., 2017). Finally, a recurring

recommendation is the urgent development expertise with technologies,

investment vehicles and transition paths.

References

Criscuolo, C., Menon, C., 2015. Environmental policies and risk finance in the green sector: Cross-country evidence. Energy Policy 83, 38–56. https://doi.org/10.1016/j.enpol.2015.03.023

Elert, N., Henrekson, M., Sanders, M., 2019. Savings, Finance, and Capital for Entrepreneurial Ventures, in: Elert, N., Henrekson, M., Sanders, M. (Eds.), The Entrepreneurial Society: A Reform Strategy for the European Union, International Studies in Entrepreneurship. Springer, Berlin, Heidelberg, pp. 53–72. https://doi.org/10.1007/978-3-662-59586-2_4

G20 Green Finance Study Group, 2016. G20

green finance synthesis report. UNEP Inquiry.

Geddes, A., Schmidt, T.S., Steffen, B., 2018. The multiple roles of state investment banks in low-carbon energy finance: An analysis of Australia, the UK and Germany. Energy Policy 115, 158–170. https://doi.org/10.1016/j.enpol.2018.01.009

La Monaca, S., Assereto, M., Byrne, J., 2018. Clean energy investing in public capital markets: Portfolio benefits of yieldcos. Energy Policy 121, 383–393. https://doi.org/10.1016/j.enpol.2018.06.028

McCollum, D.L., Zhou, W., Bertram, C., Boer, H.-S. de, Bosetti, V., Busch, S., Després, J., Drouet, L., Emmerling, J., Fay, M., Fricko, O., Fujimori, S., Gidden, M., Harmsen, M., Huppmann, D., Iyer, G., Krey, V., Kriegler, E., Nicolas, C., Pachauri, S., Parkinson, S., Poblete-Cazenave, M., Rafaj, P., Rao, N., Rozenberg, J., Schmitz, A., Schoepp, W., Vuuren, D. van, Riahi, K., 2018. Energy investment needs for fulfilling the Paris Agreement and achieving the Sustainable Development Goals. Nature Energy 3, 589–599. https://doi.org/10.1038/s41560-018-0179-z

Owen, R., Brennan, G., Lyon, F., 2018. Enabling investment for the transition to a low carbon economy: government policy to finance early stage green innovation. Current Opinion in Environmental Sustainability, Sustainability governance and transformation 2018 31, 137–145. https://doi.org/10.1016/j.cosust.2018.03.004

Polzin, F., Sanders, M., Stavlöt, U., 2018. Mobilizing Early-Stage Investments for an Innovation-Led Sustainability Transition, in: Designing a Sustainable Financial System, Palgrave Studies in Sustainable Business In Association with Future Earth. Palgrave Macmillan, Cham, pp. 347–381. https://doi.org/10.1007/978-3-319-66387-6_13

Polzin, F., Sanders, M., Täube, F., 2017. A diverse and resilient financial system for investments in the energy transition. Current Opinion in Environmental Sustainability 28, 24–32. https://doi.org/10.1016/j.cosust.2017.07.004

Röttgers, D., Tandon, A., Kaminker, C., 2018. OECD Progress Update on Approaches to Mobilising Institutional Investment for Sustainable Infrastructure. https://doi.org/10.1787/45426991-en

Bio

Friedemann

Polzin is Assistant Professor of Sustainable Entrepreneurship and Innovation at

Utrecht University School of Economics (U.S.E.) and associated researcher at

the Sustainable Finance Lab (SFL) | https://www.uu.nl/staff/FHJPolzin | https://twitter.com/friedemann_p

[1] Polzin,

F., Sanders, M., 2019. How to fill the ‘financing gap’ for the transition to

low-carbon energy in Europe? USE Discussion paper series 19-18. Available at: https://www.uu.nl/en/files/rebousewp20191918pdf