A tool to fairly distribute value and risks in the circular service economy

The earth is what we all have in common

– Wendell Berry

Do you ever try to picture how our world looks like in 30 years? Let me give you a glimpse into the circular future. In a couple of decades from now, our economic system looks fundamentally different. Healthy and resilient ecosystems will provide us with the resources we need. Yes, this is different. It will no longer be the other way around: putting our needs above the capacity of the Earth.

Matter becomes subordinate to function

We will innovate products and services to de-materialize. We will base our economic activities on what we already have and develop services and experiences based on maintaining and optimizing that. A circular company sells a service, the result of material. For example, clean & fresh laundry, instead of just a washing machine. The material that provides the result, the washing machine, remains the responsibility of the service providers. Return of material is guaranteed. The real need of the consumer is put first and not the product need. The matter becomes subordinate to the function. Yes, this is different than our current business logic, where we sell as many nearly broken products as possible.

Circular products are appreciating

Circular products are appreciating rather than depreciating. Circular products and materials can increase in value as they are enhanced and upgraded throughout their lifetime and are harvested after use. Yes, this is different. Currently, a product’s value assumes that it is trashed after its short economic life, and a new one must be bought.

Ownership will disappear

Ownership will disappear and is traded for (collective) responsibility. Responsibility for resource use and durability is placed on those that have the most influence on it. Presuming that we will still use a good old washing machine to deliver clean & fresh laundry in the future. The company that provides the motor, for example, will take responsibility for its functioning and take back. He is awarded accordingly: the longer it functions, the longer he earns from it. Yes, this is different. In the linear for sales model, as soon as materials or parts are sold, responsibility moves to the next in the chain.

Stakeholders are dependent on each other

In collective circular services, stakeholders are dependent on each other to co-provide their service; without the motor working, clean laundry can’t be delivered, and all stakeholders suffer. The circular chain is only as strong as its weakest link. Yes, this is different. In the current, linear economy, indifference and competition are the norm.

But circular frontrunners struggle to attract capital

Today, the first handful of frontrunners are already working on business models that fit this circular logic. But they are struggling to attract capital to grow their business. Current financial logic is based on linear premises: depreciating assets, growing sales targets and zero residual value. To aggravate matters, circular products must compete with cheap disposable alternatives from the linear reality where competition is the norm.

The circular distribution app is here to help

To take the first steps into the future, a consortium of financial, legal and circular inventors, came up with a new distribution app, called the circular service (CISE) platform. The CISE platform changes the relationship between service providers, consumers, and financiers fundamentally.

How does it work?

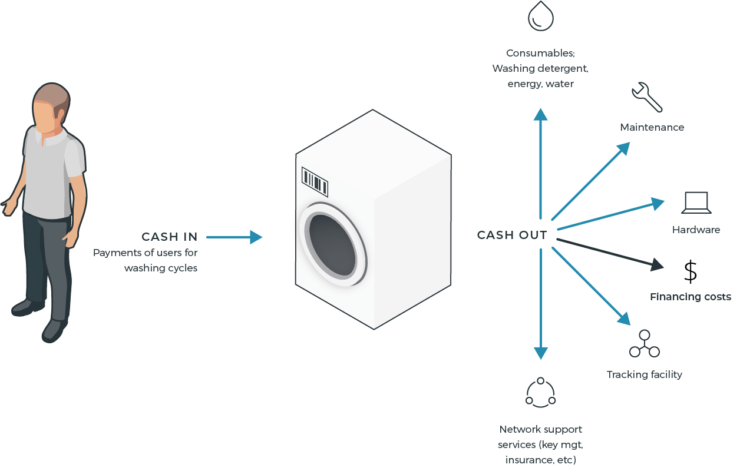

Users subscribe to a circular service, for example to a laundry service. In the CISE app, a digital wallet is created in their user accounts. All stakeholders that co-provide or co-fund the service, are connected to the circular asset, the washing machine. When the user consumes a unit of laundry, its wallet is charged. The payment is immediately distributed to all stakeholders involved without a central party coordinating.

Adapted from: Achterberg, Elisa. (2019). The Circular Service Platform [link].

How can the CISE platform improve financing circular service models?

But could CISE improve the financing of circular service companies? Are new forms of financing possible? This Community of Practice identified three ways that CiSe contributes to better financing options for the circular economy:

- Optimize existing financing models by using data. The cash flow data generated by the platform can be used to gain greater insight into usage patterns and asset performance, used for adequate cash flow projections. This can provide more certainty for financing a circular service model.

- CiSe also makes new forms of financing possible, by including the finance provider as part of the direct payment distribution. The difference is that the circular asset is financed directly, not the company. Payments are per unit of use and therefore dynamic over time and cash flows are generated over a long time.

- But financial innovation can be even more radical: circular assets can be bundled in a basket to a portfolio of x-million assets, from headphones to washing machines. The return is financed from the cash flows generated by the circular assets. CiSe could act as an investment vehicle, enabling everyone to participate in this fast-growing sector. This enables a citizen-based financial system in which users can become lenders and investors in circular assets themselves.

“We are thinking many years ahead with this. If you had asked a taxi driver what the (uber) app should look like, they could not imagine it then. For example, you cannot ask the market for the ultimate goal of CiSe, because it does not fit into an existing model. It doesn’t do something that’s already there. It’s going to do something fundamentally different.”

– Cees van Ginneken, lawyer, Allen & Overy

“I am excited by the innovative proposal that is presented in this paper. Especially about the design of the service ecosystem where everyone has a stake in successful functioning of an asset. This creates an enormous diversification opportunity: risks that are now treated per customer can be partly mitigated by the diversification.”

– Taco de Boer, New Business Manager Vendor Lease at ABN AMRO

What’s next?

There is still a giant step to be taken to get there. Together with supervisors and regulators the necessary space needs to be created to experiment with new financial models and to change the way we value circular service companies and assess their riskiness. Encouraging circular service providers to start using the CISE platform is the first step. With the data that is generated, intelligence can be developed to accurately predict cash flow patterns and create the necessary certainty for finance providers to take the plunge. Subsequently, new financial models can be structured and piloted. Eventually creating the financial models necessary for a circular future. Will you experiment with us?

“Down the rabbit hole: we just have to dive in and start by taking small steps.”

– Rob Guikers, Innovation consultant at Rabobank

To learn more on how finance could be innovated for the circular future, download the whitepaper.

This paper is a co-creation of ABN Amro, Allen & Overy, ASN Bank, Avans Hogeschool, Circle Economy, EY, 4CEE, InvestNL, Rabobank, Startgreen Capital, Stichting DOEN, Sustainable Finance Lab, UncInc, Windesheim Hogeschool and supported by Finance and the Common good.

For more information contact: Elisa Achterberg, e.achterberg@uu.nl.