A summary of Daan Bogaard’s Master’s thesis on the role of banks in the transition to regenerative agriculture

Imagine pushing your trolley through a supermarket, finding that bread and other everyday products are unavailable for days. The security you normally take for granted starts to feel less certain. While this may sound dramatic, it reflects a genuine and increasingly plausible risk.

Climate change, biodiversity loss, and soil degradation form an increasing threat to global food production. Intensive agricultural practices, while historically successful in feeding a growing population, generate environmental harm and degrade the soil quality which is essential for farming of produce. Each year, the equivalent of three billion lorry loads of fertile soil is lost worldwide.

The agriculture sector needs to transform in ways that secure long-term food security as well as reduce environmental harm. Regenerative agriculture offers a promising pathway towards more sustainable food systems, by prioritising soil health, biodiversity, and long-term resilience over short-term productivity.

In the Netherlands, 92% of agricultural debt is financed through bank loans.

However, farmers face barriers when transitioning away from intensive to regenerative practices. The characteristics of the Dutch agriculture sector – intensive land use, high land prices, and a strong export-oriented model – makes the transition particularly challenging. In theory, banks have the potential to act as enablers of sustainability transitions by directing capital flows, providing appropriate financing, and designing financial products that incentivise change. In the Netherlands, their role is especially important, as 92% of agricultural debt is financed through bank loans. Despite their potential, research on finance’s role in sustainability transitions remains limited. Understanding how banks can facilitate this transition to regenerative agriculture is therefore essential.

SFL and agriculture: not an obvious match

The Sustainable Finance Lab is part of the Dutch national programme ReGeNL, which aims to kick-start the transition towards a future-proof agricultural sector. The project runs until the end of 2030. Together with wide range of partners across the agriculture sector, ReGeNL supports farmers in their transition to regenerative agriculture. At the same time, the programme studies the broader transition from multiple perspectives, spanning individual farmers to the wider food system, and across different levels, including business models, measurement frameworks, and human capital. Within ReGeNL, we focus on translating academic knowledge into practice, connecting and convening academia, policymakers, and the financial sector, and studying new financing models (for area-based transitions).

Interconnected systemic risks of nature and biodiversity loss stemming from intensive agriculture make the transition highly relevant for financial institutions. Addressing these risks aligns with SFL’s mission to contribute to a just financial system that serves both society and the planet.

Barriers to financing regenerative agriculture

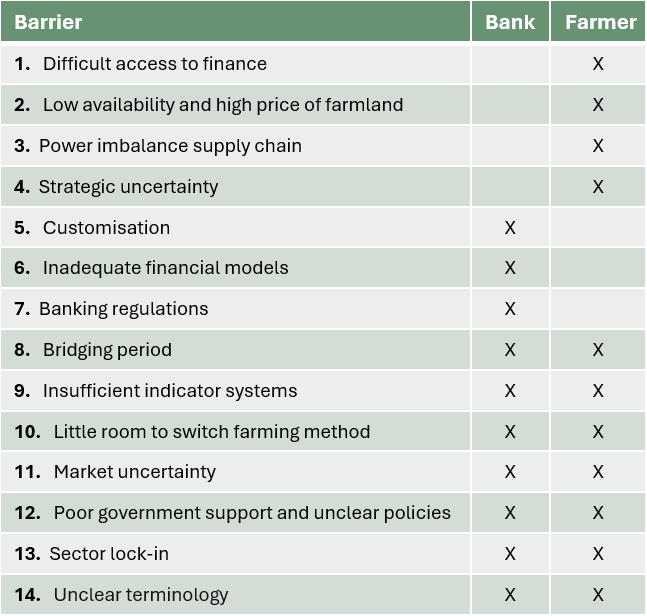

We have identified fourteen barriers to financing the regenerative agriculture transition, affecting banks, farmers, or both. A number of these are covered below.

A transitioning farm typically experiences a bridging period in the first years, where income and yield decline. Farmers then struggle to meet financial requirements and this uncertainty makes banks reluctant to provide finance. A lack of universally accepted indicators prevents banks and farmers from legitimising a regenerative business model.

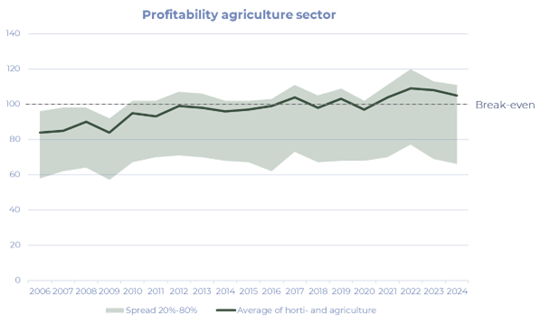

Farms have seen very low profitability over the years. Market power lies predominantly elsewhere in the chain, allowing these parties to capture a large share of the margin. Farms are unattractive investments due low return, leaving farmers with little resources to make the transition.

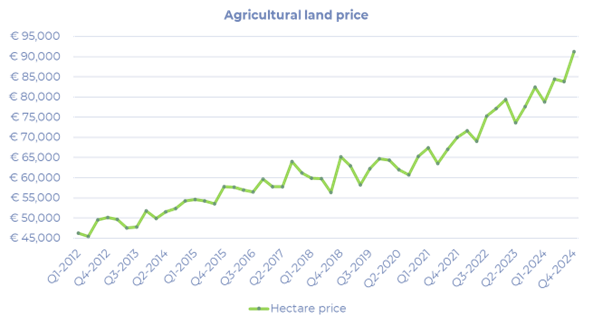

In addition, land prices have doubled in the last twelve years and are eight times the European average, while farmers depend on acquiring new farmland to extensity. The complexity of the land market and its underlying price drivers requires a comprehensive financial analysis to fully understand the issue.

Once farmers have made the transition, regenerative products often face low consumer demand. This market uncertainty limits profit opportunities. At the same time, higher prices are needed to compensate for transition costs, and a viable market is an important condition for securing bank financing.

What role can banks play?

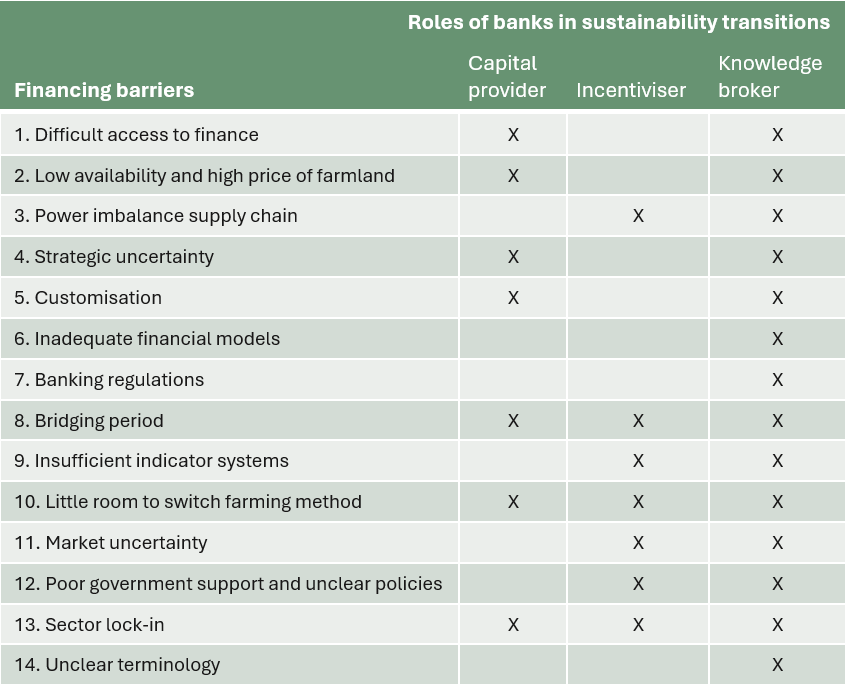

Banks can facilitate the transition by playing (at least) three roles: as capital provider, as incentiviser, and as knowledge broker. Steering capital flows towards sustainable investments should be the most obvious role. They can provide capital and enable investments for regenerative farmers. Secondly, banks can promote regenerative practices by designing financial instruments that give financial incentives. For instance, a discounted interest rate on regenerative loans. Lastly, banks gather a lot of information about the agriculture sector, which creates an opportunity to distribute knowledge about regenerative agriculture within the sector, offer advice and initiate new ideas. Banks can leverage their extensive networks to connect key stakeholders, helping to coordinate the transition and increase its chances of success.

Then again, banks face constraints that hinders these roles. The financial regime has a slow-moving nature and is characterised by institutional inertia, including a risk-return focus, limited customisation, less adapted risk models and a short time horizon. Banks’ focus is typically on risk-return, where the lowest possible risk should yield the highest possible return. This is less compatible with investing in a regenerative agriculture transition, where risk and uncertainty are inherent. Bank financing typically requires scalability to fit institutional processes, yet the agricultural sector is far from homogenous. The required customisation limits their ability to finance regenerative agriculture on a large scale. Current risk models are often lagging in their development. They are less adapted to new forms of agriculture or regional differences and are often still based on the intensive model. Finally, targets and profits must be achieved in the short term. Since regenerative returns only become visible in the long term, the banks’ time horizon is not always aligned with the transition.

Banks can help farmers absorb operational risks of switching farming methods and create space for vital investments in regenerative practices.

A cross-analysis demonstrates how each bank’s role can address specific barriers, offering a clearer understanding of how banks can effectively support the transition. By offering favourable terms, such as flexible repayments and interest rate reductions, banks can help farmers absorb operational risks of switching farming methods and create space for vital investments in regenerative practices. Public-private blended finance (i.e. guarantees or outcome-based contracts) can be used to further de-risk the bridging period and unlock the sector lock-in.

Banks can share transition cases and present replicable switching methods, acting as learning hubs and empower farmers to move towards regenerative practices. Banks can drive standardisation of indicators, adequate financial models and clear terminology, by convening initiatives with certification bodies, research institutes (e.g. Wageningen University), and other actors within their network. This role as knowledge broker not only benefits the agricultural sector externally; it also reinforces banks’ internal operations. It could help educate internal risk teams about non-financial benefits (e.g. soil health) and align loan assessment with sustainability metrics. Banks can help regulators and policy makers by flagging financial bottlenecks, advocating for more enabling conditions for regenerative practices and public-private coordination to address the poor government support.

The road ahead: financing a resilient food system

While banks have a supporting role to play in facilitating the transition, transforming food systems requires collective effort across the whole public and private sector. Despite ecological, economic, and social benefits, aligning financial instruments with the financing needs of regenerative farms remains challenging.

At the Sustainable Finance Lab, we will explore how the financial sector can be better enabled to support this transition. This entails examining what types of capital are required to finance regenerative farms effectively, which financial actors should be involved, and which existing or new financial instruments could help bridge the current financing gap.

Ultimately contributing to the regenerative farming transition that makes the food system sustainable and more resilient to disruptive events. Ensuring that the unsettling experience of pushing a trolley past empty shelves remains the exception rather than the norm.